The U.S. Secretary of Labor Thomas E. Perez

wants to raise the minimum wage.

In fact,

the vast majority of Americans -- 91 percent of Democrats, but also 76

percent of Independents and even 58 percent of Republicans -- are in

favor of raising the minimum wage.

This is an

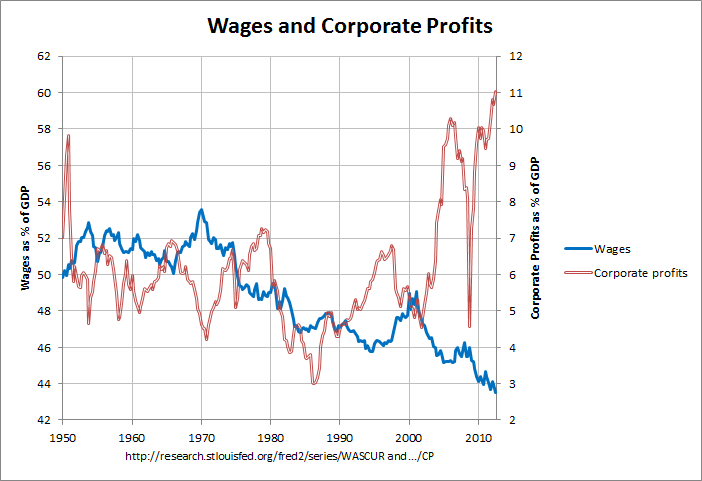

understandable position. After all, the gap between richest and poorest

has grown very wide in recent years. But in my view, minimum wage laws

are not good laws at all. That’s not out of lack of compassion for

low-wage earners, or because I like inequality. That is because I think

that there is

a better way to achieve a decent standard of living for

the poorest in society.

The minimum wage is a factor in creating unemployment. Despite what's often said to the contrary, it's true:

Countries with no minimum wage tend to have much lower unemployment. Right now, America is suffering a serious deficit of jobs,

with over three jobseekers for every available job. We need all the jobs we can get.

So

how does

the minimum wage create unemployment? Minimum wage laws are a price

control. They dictate the minimum level that a company can pay a worker.

If the minimum wage is $10, and a company wants to take on a new

employee that they determine will be worth $8 an hour, they have a

choice -- either pay $10 an hour, or not hire the employee. Sometimes,

the company will accept a hit to their profit margin, and pay the

employee $10 an hour.

Sometimes they will just not

hire a new employee at all. Or, increasingly, sometimes they will go

overseas and hire an employee elsewhere -- like China -- where wages are

far lower. This is a particularly cruel scenario because it

discriminates most against the poorest and youngest workers in society.

Empirically,

the minimum wage has failed to reach its goal of ensuring a fair wage

for low wage workers. Worker productivity in America has risen and

risen, yet the minimum wage has not.

I propose abolishing the minimum wage, and replacing it with a

basic income policy, a version of which was first advocated in America by

Thomas Paine.

Individuals would be able to work for whatever wage they can secure,

meaning that low-skilled individuals -- especially the young,

who currently face a particularly high rate of employment

-- would have an easier time finding work. And the level of basic

income could be tied to the level of productivity, to reduce inequality.

There

are two kinds of basic income policy. The first is a negative income

tax -- if an individual’s income level falls beneath a certain threshold

(say, $1,500 a month) the government makes up the difference. Funds for

this could be accessed by consolidating existing welfare programs like

state-run pension schemes and unemployment benefits, and by closing tax

loopholes and raising taxes on

corporate profits and high-income earners. Germany has enacted a similar policy -- called the

"Kurzabeit"

-- and it's been credited with shielding the German labor force from

the worst of the recession and keeping their unemployment rate low

since.

The second is a universal income policy, where

everyone receives a payment irrespective of their income. This would

obviously require more funds -- meaning higher taxes -- but in a future

where corporations are making larger and larger profits while requiring

fewer and fewer workers

due to automation, such policies may become increasingly feasible. There are already very serious proposals to initiate such a scheme

in Switzerland.

*** [12/18/13 Cramer on the minimum wage]

When I first broke in at

Goldman Sachs (GS +2.55%)

in the early 1980s, I was in charge of tabulating turnover in what was

then known as the Securities Sales Department. It was my job to keep

track of who stayed and who went, and to be sure I knew the details of

each departure. I was told that, historically, Goldman Sachs tried hard

not to lose anyone it wanted to keep, even as it was willing to see the

others depart -- and, for the time when I did the tallying, the

division's record was perfect on that score.

When I was

first assigned the project, I had no idea why it was so important to

keep track of how few people actually left the firm, other than for

boasting rights vs. the competition, which always seemed to be losing

people left and right.

But once I was in the fold, I

realized the reason Goldman closely observed this number had to do with

the tremendous cost of training people, and how departures -- any

departures, of good people -- meant a total loss on an important

human-capital investment.

In the division in which I

worked, Goldman Sachs aspired for zero turnover because the firm spent,

on average, six months teaching associates how to do their job -- and,

during that period, these trainees were dead-weight losses to the firm.

Trainees were sunk costs; you couldn't afford to lose the good ones. It

could really hurt your firm's P&L, or profit and loss statement.

Few

issues could be more bedeviling to profitability than turnover, and

Goldman Sachs did everything it could to discourage it, including paying

people more, teaching people better and offering them more benefits

than you could get elsewhere.

It worked. The firm was by

far the most lucrative investment house on Wall Street then, and to a

large extent it still is now, perhaps because it maintains an excellence

in training.

Now fast-forward to Tuesday's interview with John Mackey and Walter Robb, co-CEOs of

Whole Foods (WFM +0.44%), at the opening of their Brooklyn store.

Both

execs spoke intently and intensely about how turnover is the bane of

their existence because it hurts all stakeholders, the remaining

associates and managers left behind, the customers and the shareholders.

In their opinion,

paying people much more than the minimum wage, while

offering them some of the best perks and benefits in the retail world,

has led to a remarkable cost

advantage -- not disadvantage -- vs.

many retailers, where the goal seems to be to squeeze as much out of

their workers as possible. Mackey and Robb know there's a big cost to

the firm when people leave. They know that turnover is a killer to the

bottom line.

{kind=link}