People usually get better at things over time. We're better farmers,

faster runners, safer pilots, and more accurate weather forecasters than we were 50 years ago.

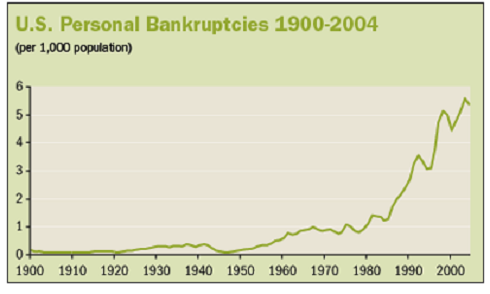

But there's something about money that gets the better of us. If you look at

the rate of

personal bankruptcies, financial crises, bubbles, student loans, debt

defaults, and savings rates, I wonder whether people are just as bad at

managing money today as they were in previous generations, maybe even

worse. It's one of the only areas in life we seem to get progressively

dumber at.

Here are

77 reasons why people are awful at managing money.

3. You suffer from the

Dunnig-Kruger effect,

lacking enough basic financial knowledge to even realize that you're

making mistakes. People's lack of understanding about things like

compound interest and inflation can lead them to believe they're making

good financial decisions when in reality they're tripping over

themselves with failure.

4. For every $1 raise you receive, your desires rise by $2 or more.

5. You spend lots of money on material stuff to impress other people

without realizing those other people couldn't care less about you. You'd

be shocked at how few people care where your purse was made or how much

noise your car makes.

13. The single largest expense you'll pay in life is interest. You'll

spend more money on interest than food, vacations, cars, school,

clothes, dinners out, and all forms of entertainment. You do this

because you don't save enough and demand a lifestyle you can't actually

afford. The future owns your income.

14. You're thrilled that the credit card you're paying 22% interest on offers 1% cash back on all purchases.

15. You spent the last five years arguing why Keynesian/Austrian economists were all wrong. The

S&P 500 (

SNPINDEX: ^GSPC ) spent the last five years rallying 177%.

16. You think dollar-cost averaging is boring without realizing that

the purpose of investing isn't to minimize boredom; it's to maximize

returns.

17. Your work in a stressful job in order to make enough money to have a stress-free life. You see no irony in this.

18. You're a pessimist in a world where far more

people wake up in the morning trying to make things better than wake up

thinking we're all doomed.

19. You try to keep up with the Jonses without realizing the Jonses are buried in debt and can probably never retire.

21. You associate all of your financial successes with skill and all of your financial failures with bad luck.

22. Rather than admitting and learning from your mistakes, you ignore

them, bury them, make excuses for them, and blame them on others.

23. You anchor to whatever price you bought a stock for, without

realizing that the market neither knows nor cares what you think is a

"fair" price.

27. You say you'll be greedy when others are fearful, then seek the fetal position when the market falls 2%.

30. You let confirmation bias take control of your

mind by only seeking out information from sources that agree with your

pre-existing beliefs.

31. You think you're too young to start saving for retirement when

every day that passes makes compound interest a little bit less

effective.

32. You spend a month researching the best washing machine, then

invest twice as much money in a penny stock based solely on a tip from a

person you don't know and shouldn't trust.

33. You're investing for the next 50 years but get stressed when the market has a bad day.

34. You're willing to work hard for $15 an hour, but too lazy to

spend four minutes to fill out your company's 401(k) paperwork that

could result in thousands of dollars of free money from matching

contributions.

39. You don't respect the idea that "do nothing" are two of the most powerful words in investing.

41. You feel especially smart after last year's 30% market rally without realizing that you had nothing to do with it.

42. You surround yourself with 18 hours a day of live market TV in a

game that requires decades of doing almost nothing but waiting.

45. You think financial news is published because it has useful

information you need to know. In reality, it's published only because

the publisher knows you'll read it.

46. You forget that the single most valuable asset you have as an

investor is time. A 20-year-old has an asset Warren Buffett couldn't

dream about.

50. You think it's impossible to live on less than $35,000 a year

without realizing that literally 99% of the world does, even adjusted for purchasing power parity.

51. Your definition of a middle-class lifestyle is a 3,000-square

foot home, more bathrooms than family members, three SUVs, private

colleges, annual trips to Hawaii and Vail, Evian water, and yoga

lessons. (Seriously, just stretch in your own living room.)

52. You can't acknowledge the role luck plays when making the

occasional successful investment. (Also true when worshiping investors

who made one big call that happened to be right.)

53. You suffer from hard-core belief bias. It's the tendency to

accept or reject an argument based on how well it fits your pre-defined

beliefs, rather than the objective facts of the situation. Pointing out

that inflation has been low for the last five years is still met with

suspicion by those who believe the Federal Reserve's actions must be

causing hyperinflation.

56. You think the stock market is too risky because it's volatile,

without realizing that the biggest risk you face isn't volatility; It's

not growing you assets by enough over the next several decades.

57. You've never been to a poor country, robbing you of the

realization that the world doesn't care how entitled you feel, what you

think is "fair," or what a real financial hardship is.

58. You think blowing money on frivolous stuff impresses people, when

in reality it makes you look like an insecure, pompous, jerk. (This is

particularly common among young people who come into money for the first

time.)

59. You're unable to realize that a 10% return for 20 years generates

more money than a 20% return for 10 years. Time can be a more important

factor than return when building wealth -- and it's the one thing you

have control over.

60. You don't respect the mountains of evidence showing that once

basic needs are met, the amount of happiness each additional dollar of

income provides diminishes quickly. This causes you to spend most of

your life chasing "the number" you think will make you happy, but

probably won't.

62. You think of the stock market as numbers that go up and down

rather than an ownership stake in real businesses with real assets.

63. You think renting a home is throwing money away

when for many it's one of the smartest financial decisions they can make.

64. Your investment decisions are guided by what the economy is doing, when the two really

have very little correlation.

66. You're unable to have a good time going for a hike, a bike ride, a

swim, reading a book, or anything else that's free (or cheap). Having

cheap hobbies is a large, yet hidden, asset on your personal balance

sheet.

68. To paraphrase Carl Richards, you ignore history, basing your actions on your own very limited experience.

71. You think that not changing your opinion about markets, the

economy, and your investments is somehow noble, when it's really just

shutting your brain off to the reality that things are always changing.

72. You ignore that how elderly Americans who have seen it all

view money is almost the opposite of how most young Americans view money. This goes back to not learning vicariously.

74. You underestimate how fast a company can go from "blue chip" to bankrupt.

75. You don't realize that when you say you want to be a millionaire,

what you probably mean is that you want to spend a million dollars,

which is literally the opposite of being a millionaire.

76. You're unaware that the business models of the vast majority of

financial companies rely on exploiting the fears, emotions, and lack of

intelligence of its customers.

77. You nodded along to all 77 of these points without realizing I'm talking about

you. That goes for me, too.

{kind=link}