Morgan Stanley (MS) will buy E-Trade Financial (ETFC) in an all-stock deal valued at $13 billion as online brokers have cut stock and ETF trading commissions to $0.

The E-Trade deal comes on the heels of another major acquisition in the brokerage space. Last November, larger brokerage rivals Charles Schwab (SCHW) and TD Ameritrade (AMTD) agreed to merge in a $26 billion, all-stock deal.

Under the terms of the latest deal, Morgan Stanley will pay $58.74 per E-Trade share. The deal is expected to close in the fourth quarter.

"E-Trade represents an extraordinary growth opportunity for our wealth management business and a leap forward in our wealth management strategy," said Morgan Stanley CEO James Gorman, in the press release. "In addition, this continues the decade-long transition of our firm to a more balance sheet light business mix, emphasizing more durable sources of revenue."

The combined company will have $3.1 trillion in client assets 8.2 million retail client relationships and accounts, and 4.6 million stock plan participants, according to Morgan Stanley.

Thursday, February 20, 2020

Saturday, February 15, 2020

dead investing

Google "Fidelity dead investors" and you'll see a number of stories come up. The Conservative Income Investor informs that when conducting an internal performance review of customer performance from 2003 to 2013, Fidelity learned that those with the best returns were "either dead or inactive." Hedge fund manager Mohnish Pabrai refers to that study in a speech. In June, Moneyvator.com upgraded the finding's status to public, writing that Fidelity had "released a study" to that effect.

Well, maybe. My Fidelity contact has not heard of such a thing, nor has Morningstar's Fidelity Canada contact. Suffice it to say that none of these citations came linked to the original source. (Such is the Internet.)

However, the general notion is sound. As William Sharpe explained decades ago, and institutional investors have learned to believe fervently (no split infinitives here!), investing is a zero-sum game. One side wins on a trade, the other does not. More trades lead to more costs, which must be overcome by notching more than one's share of wins. Sure, that can happen. But for a great number of investors, on average? Highly unlikely.

Even if Fidelity's retail customers trade as well as professionals, and are not beaten in aggregate by portfolio managers, as a group they don't figure to overcome the friction caused by trading costs.

Well, maybe. My Fidelity contact has not heard of such a thing, nor has Morningstar's Fidelity Canada contact. Suffice it to say that none of these citations came linked to the original source. (Such is the Internet.)

However, the general notion is sound. As William Sharpe explained decades ago, and institutional investors have learned to believe fervently (no split infinitives here!), investing is a zero-sum game. One side wins on a trade, the other does not. More trades lead to more costs, which must be overcome by notching more than one's share of wins. Sure, that can happen. But for a great number of investors, on average? Highly unlikely.

Even if Fidelity's retail customers trade as well as professionals, and are not beaten in aggregate by portfolio managers, as a group they don't figure to overcome the friction caused by trading costs.

Wednesday, February 05, 2020

who benefits from the stock market?

(Reuters) - Donald Trump loves to trumpet the hot U.S. stock market as a key achievement of his presidency, and he was in full self-congratulatory mode on that front during Tuesday night’s State of the Union address.

“All of those millions of people with 401(k)s and pensions are doing far better than they have ever done before with increases of 60, 70, 80, 90 and 100 percent and even more,” Trump said in his address to a joint session of Congress.

While pensions and retirement funds were lifted by the rise in stock markets, the president has avoided talking about one key point about who really benefits when the market rallies: Most of the gains go to the small portion of Americans who are already rich.

That’s because 84% of stocks owned by U.S. households are held by the wealthiest 10% of Americans, according to an analysis of 2016 Federal Reserve data by Edward Wolff, an economics professor at New York University. So when the stock market has a blockbuster year - such as the nearly 30% rise in the S&P 500 benchmark index in 2019 - the payoff primarily goes to people who are already rich.

“For most Americans, a stock price increase is pretty immaterial to their well-being,” said Wolff, who published a paper about wealth inequality in the National Bureau of Economic Research in 2017.

Roughly half of Americans own some stocks through a brokerage account or a pension or retirement fund. But for most people, the exposure is too small for market gains to be life-changing or leave them feeling much better about their finances, Wolff said. “They’ll see a small increase in their wealth, but it’s not going to be anything to write home about,” he said.

What’s more, nearly 90% of families who own stock do so through a tax-deferred retirement account, meaning they can’t access the money until they reach retirement age, unless they pay a penalty, Wolff said.

“All of those millions of people with 401(k)s and pensions are doing far better than they have ever done before with increases of 60, 70, 80, 90 and 100 percent and even more,” Trump said in his address to a joint session of Congress.

While pensions and retirement funds were lifted by the rise in stock markets, the president has avoided talking about one key point about who really benefits when the market rallies: Most of the gains go to the small portion of Americans who are already rich.

That’s because 84% of stocks owned by U.S. households are held by the wealthiest 10% of Americans, according to an analysis of 2016 Federal Reserve data by Edward Wolff, an economics professor at New York University. So when the stock market has a blockbuster year - such as the nearly 30% rise in the S&P 500 benchmark index in 2019 - the payoff primarily goes to people who are already rich.

“For most Americans, a stock price increase is pretty immaterial to their well-being,” said Wolff, who published a paper about wealth inequality in the National Bureau of Economic Research in 2017.

Roughly half of Americans own some stocks through a brokerage account or a pension or retirement fund. But for most people, the exposure is too small for market gains to be life-changing or leave them feeling much better about their finances, Wolff said. “They’ll see a small increase in their wealth, but it’s not going to be anything to write home about,” he said.

What’s more, nearly 90% of families who own stock do so through a tax-deferred retirement account, meaning they can’t access the money until they reach retirement age, unless they pay a penalty, Wolff said.

Tuesday, January 28, 2020

U.S. budget deficit to top $1 trillion

WASHINGTON (Reuters) - The U.S. economy will grow at a “solid” rate of 2.2% this year, the non-partisan Congressional Budget Office forecast on Tuesday, but the federal budget deficit will hit $1.02 trillion.

The economy will be strong during this presidential election year, thanks in part to consumer spending, CBO said, but it forecast “higher inflation and interest rates after a decade in which both remained low, on average.”

Economic growth will slow to an average annual rate of 1.7% from 2021 to 2030, CBO predicted, while inflation and interest rate increases will slow in 2023.

After topping $1 trillion in fiscal 2020, federal deficits will average $1.3 trillion per year between 2021 and 2030, CBO estimates, a level that some economists and policymakers warn is unsustainable.

Washington’s budget deficit hit a peak of $1.4 trillion in fiscal 2009, after emergency measures to contain a severe economic recession that began two years earlier.

It hasn’t topped $1 trillion since 2012 and fell to $585 billion at the end of President Barack Obama’s second term in 2016.

The current and forecast deficits come under better economic circumstances, but after a Republican overhaul of the tax system, which reduced revenues over the short term. Federal outlays in 2020 will be $4.6 trillion, while revenues will hit $3.6 trillion, CBO estimates.

CBO projections assume that current laws governing taxes and spending will generally remain unchanged.

Under the current system, budget deficits will push overall U.S. federal debt held by the public to $31.4 trillion by the end of 2030, CBO estimated.

That would be 98% of gross domestic product, or the total monetary value of all goods and services produced in the United States. That’s a higher rate than at any point since just after World War II, CBO said, and “more than double what it has averaged over the past 50 years.”

Interest payments on federal debt, coupled with increased spending on mandatory federal programs like Social Security, will be the biggest contributors to climbing federal outlays in coming decades, the CBO said.

As a result, U.S. federal spending will grow more than revenues through 2050, CBO estimates.

The economy will be strong during this presidential election year, thanks in part to consumer spending, CBO said, but it forecast “higher inflation and interest rates after a decade in which both remained low, on average.”

Economic growth will slow to an average annual rate of 1.7% from 2021 to 2030, CBO predicted, while inflation and interest rate increases will slow in 2023.

After topping $1 trillion in fiscal 2020, federal deficits will average $1.3 trillion per year between 2021 and 2030, CBO estimates, a level that some economists and policymakers warn is unsustainable.

Washington’s budget deficit hit a peak of $1.4 trillion in fiscal 2009, after emergency measures to contain a severe economic recession that began two years earlier.

It hasn’t topped $1 trillion since 2012 and fell to $585 billion at the end of President Barack Obama’s second term in 2016.

The current and forecast deficits come under better economic circumstances, but after a Republican overhaul of the tax system, which reduced revenues over the short term. Federal outlays in 2020 will be $4.6 trillion, while revenues will hit $3.6 trillion, CBO estimates.

CBO projections assume that current laws governing taxes and spending will generally remain unchanged.

Under the current system, budget deficits will push overall U.S. federal debt held by the public to $31.4 trillion by the end of 2030, CBO estimated.

That would be 98% of gross domestic product, or the total monetary value of all goods and services produced in the United States. That’s a higher rate than at any point since just after World War II, CBO said, and “more than double what it has averaged over the past 50 years.”

Interest payments on federal debt, coupled with increased spending on mandatory federal programs like Social Security, will be the biggest contributors to climbing federal outlays in coming decades, the CBO said.

As a result, U.S. federal spending will grow more than revenues through 2050, CBO estimates.

Friday, January 17, 2020

longest bull market

With the most recent SPX high on Thursday (1/16), below is an update of the table illustrating how this bull market compares to others in the post WW II era. At 3,964 days in duration, it is now 513 days longer than the internet bull market, but at +390%, it remains second highest with regard to the percentage increase. The SPX would need to reach a level of about 3,500 to exceed the 417% gain of the strongest bull market in history. This would only be a 2020 YTD gain of about +8.5% if it happened by the end of 2020.

With about 10 months still to go in his first term, President Trump has moved solidly into 4th place overall for market performance in the post WW II era (surpassing Bush #41 last week). As of Thursday (1/16) the SPX is +55.0% since Election Day 2016. It’s a long road to the next position (Clinton +70.1%) but it is not unrealistic to think the SPX could reach 3,641 before Election Day 2020, if the bull market continues. That would equate to less than a 13% YTD gain.

{kind=link}

With about 10 months still to go in his first term, President Trump has moved solidly into 4th place overall for market performance in the post WW II era (surpassing Bush #41 last week). As of Thursday (1/16) the SPX is +55.0% since Election Day 2016. It’s a long road to the next position (Clinton +70.1%) but it is not unrealistic to think the SPX could reach 3,641 before Election Day 2020, if the bull market continues. That would equate to less than a 13% YTD gain.

{kind=link}

Thursday, January 16, 2020

Ben Graham

[1/22/20] The Benjamin Graham breakthrough

[7/8/15] 15 Thoughts from Grandmaster Ben Graham

[8/17/06] Foolish Book Review: The Intelligent Investor

[8/11/06] Ben Graham's equation<!- via Rick Daley value_investment_thoughts-->

[11/12/05] brknews passes along this article by Sanjay Bakshi who writes about Graham's rule of minimum valuation.

[11/9/05] Shai has generously passed me more items on Ben Graham from his blog.

[11/7/05] Graham's simple rules

[10/18/05] Two lessons from Benjamin Graham

[8/6/05] Ben Graham is still pointing the way

[8/6/05] A test of Graham's stock selection criteria

[8/5/05] Graham's Net Current Asset Value Strategy (dryice's follow up)

[8/4/05] High Performance Graham Stocks (a Ben Graham screen)

[8/3/05] Graham favored two methods: buying stocks that were selling substantially below the value of their assets, and selecting companies that boasted consistent earnings and solid financial foundations.

[7/8/15] 15 Thoughts from Grandmaster Ben Graham

[8/17/06] Foolish Book Review: The Intelligent Investor

[8/11/06] Ben Graham's equation<!- via Rick Daley value_investment_thoughts-->

[11/12/05] brknews passes along this article by Sanjay Bakshi who writes about Graham's rule of minimum valuation.

[11/9/05] Shai has generously passed me more items on Ben Graham from his blog.

[11/7/05] Graham's simple rules

[10/18/05] Two lessons from Benjamin Graham

[8/6/05] Ben Graham is still pointing the way

[8/6/05] A test of Graham's stock selection criteria

[8/5/05] Graham's Net Current Asset Value Strategy (dryice's follow up)

[8/4/05] High Performance Graham Stocks (a Ben Graham screen)

[8/3/05] Graham favored two methods: buying stocks that were selling substantially below the value of their assets, and selecting companies that boasted consistent earnings and solid financial foundations.

Sunday, January 12, 2020

A prediction for 2020

It is the time of year for predictions and I’ll make one: You will be better off ignoring the Wall Street stock-market predictions for 2020.

Strategists, some of whom are very smart, are issuing precise predictions for where the market will be in 12 months and they look authoritative.

The record shows that they are not as rock-solid as they appear.

In fact, many Wall Street strategists are flagrantly inaccurate. They are about as reliable as a weather forecaster who always calls for balmy sunshine in a city where it rains or snows a lot. It is true that they are right about the market’s direction more often than they are wrong. But that’s only because most of them say the market will rise in the next year, which happens about 70 percent of the time.

The more specific forecasts — like how high or low the market will go in a given year, and whether it will lose half of its value or rise 30 percent — should be treated as fiction.

I’m not exaggerating.

Paul Hickey, a co-founder of Bespoke Investment Group, crunched the numbers for me, updating calculations that I cited four years ago. Sadly, the forecasters are no more impressive now than they were then.

For every calendar year since 2000, Mr. Hickey compared the annual Wall Street consensus forecast in late December with the actual level of the S&P 500 one year later. He found that, on average:

The median forecast was that the stock index would rise 9.8 percent in the next calendar year. The S&P 500 actually rose 5.5 percent.

The gap between the median forecast and the market return was 4.31 percentage points, an error of almost 45 percent.

The median forecast was that stocks would rise every year for the last 20 years, but they fell in six years. The consensus was wrong about the basic direction of the market 30 percent of the time.

Mr. Hickey found that the forecasts were often off by staggering amounts, especially when an accurate forecast would have mattered most. In 2008, for example, when stocks fell 38.5 percent, the median forecast was typically cheery, calling for an 11.1 percent stock market rise. That Wall Street consensus forecast was wrong by 49.6 percentage points, and it had disastrous consequences for anyone who relied on it.

But there is a more reliable and a simpler way to make investing decisions, one that doesn’t rely on putative forecasts. It is based instead on long-term historical data on the broad returns of the stock and the bond markets.

They show that stocks outperform bonds over extended periods, but that stocks are far more volatile than bonds. Holding both stocks and bonds makes sense because they tend to buffer one another.

Investing over the long run through low-cost index funds in a broadly diversified portfolio is a reasonable approach for most people. This is standard wisdom among many experienced hands in investing, and Jack Bogle, the founder of Vanguard, made it a viable strategy for great masses of people by starting the first commercially available index fund. Of course, Warren Buffett recommends this approach. And so does David Booth, the co-founder of the firm Dimensional Fund Advisors and the benefactor for whom the University of Chicago Booth School of Business is named.

Mr. Booth doesn’t make market forecasts, nor does his company, which was built on the research of economists like Eugene Fama, a Nobel laureate in economics at the University of Chicago.

“We don’t try to forecast the future,” Mr. Booth told me in a recent conversation. “We have no ability to do it. Nor does anyone else.”

Instead, Mr. Booth says, forget the forecasts — and, for the purpose of investing, forget about the current news, too. He doesn’t recommend picking individual stocks or bonds.

Keep it simple, he said, and don’t try to outsmart the market. Take on only as much risk you can handle.

“When you have some money to invest, put it into low-cost, diversified index funds,” he said. “Find a stock-bond mix that you are comfortable with. And if you realize you’re not comfortable, change it until you are — and then stick with it for years, and do better things with your life than worrying about where the market is going.”

One way of thinking about risk is to imagine that a terrible downturn is about to occur, he said. “It will happen, if you live long enough. You can count on that.”

If you are a conservative, older investor, as he is, he said, you might consider a portfolio with 25 percent stocks and 75 percent bonds.

Consider the worst stock downturn in our lifetimes, from October 2007 through February 2009, he said.

In that horrendous period, when global markets fell 55 percent, this hypothetical conservative portfolio would have lost about 13.5 percent — and recovered all of the lost ground within 7 months. “When you look at the numbers,” he said, “you may think, ‘I can deal with that and sleep at night.’”

If you are younger or more aggressive in your investing, though, you might want to try a portfolio with more stock in it — say, 60 percent stock, with the remainder in bonds. But be aware that in the 2007-2009 market catastrophe, that portfolio would have lost about 35.6 percent and have required two years to recover entirely.

Because the bond market has been unusually strong, the conservative portfolio gained about 5.2 percent, annualized, over the 20 years through September; the more aggressive one gained slightly more, about 5.3 percent.

There are, of course, no guarantees that these returns will be duplicated in the future, Mr. Booth said.

“What this is, I think, is a reasonable approach to the future, based on the record of the past,” he said.

One thing it is not is a forecast.

-- Jeff Sommer, New York Times

Strategists, some of whom are very smart, are issuing precise predictions for where the market will be in 12 months and they look authoritative.

The record shows that they are not as rock-solid as they appear.

In fact, many Wall Street strategists are flagrantly inaccurate. They are about as reliable as a weather forecaster who always calls for balmy sunshine in a city where it rains or snows a lot. It is true that they are right about the market’s direction more often than they are wrong. But that’s only because most of them say the market will rise in the next year, which happens about 70 percent of the time.

The more specific forecasts — like how high or low the market will go in a given year, and whether it will lose half of its value or rise 30 percent — should be treated as fiction.

I’m not exaggerating.

Paul Hickey, a co-founder of Bespoke Investment Group, crunched the numbers for me, updating calculations that I cited four years ago. Sadly, the forecasters are no more impressive now than they were then.

For every calendar year since 2000, Mr. Hickey compared the annual Wall Street consensus forecast in late December with the actual level of the S&P 500 one year later. He found that, on average:

The median forecast was that the stock index would rise 9.8 percent in the next calendar year. The S&P 500 actually rose 5.5 percent.

The gap between the median forecast and the market return was 4.31 percentage points, an error of almost 45 percent.

The median forecast was that stocks would rise every year for the last 20 years, but they fell in six years. The consensus was wrong about the basic direction of the market 30 percent of the time.

Mr. Hickey found that the forecasts were often off by staggering amounts, especially when an accurate forecast would have mattered most. In 2008, for example, when stocks fell 38.5 percent, the median forecast was typically cheery, calling for an 11.1 percent stock market rise. That Wall Street consensus forecast was wrong by 49.6 percentage points, and it had disastrous consequences for anyone who relied on it.

But there is a more reliable and a simpler way to make investing decisions, one that doesn’t rely on putative forecasts. It is based instead on long-term historical data on the broad returns of the stock and the bond markets.

They show that stocks outperform bonds over extended periods, but that stocks are far more volatile than bonds. Holding both stocks and bonds makes sense because they tend to buffer one another.

Investing over the long run through low-cost index funds in a broadly diversified portfolio is a reasonable approach for most people. This is standard wisdom among many experienced hands in investing, and Jack Bogle, the founder of Vanguard, made it a viable strategy for great masses of people by starting the first commercially available index fund. Of course, Warren Buffett recommends this approach. And so does David Booth, the co-founder of the firm Dimensional Fund Advisors and the benefactor for whom the University of Chicago Booth School of Business is named.

Mr. Booth doesn’t make market forecasts, nor does his company, which was built on the research of economists like Eugene Fama, a Nobel laureate in economics at the University of Chicago.

“We don’t try to forecast the future,” Mr. Booth told me in a recent conversation. “We have no ability to do it. Nor does anyone else.”

Instead, Mr. Booth says, forget the forecasts — and, for the purpose of investing, forget about the current news, too. He doesn’t recommend picking individual stocks or bonds.

Keep it simple, he said, and don’t try to outsmart the market. Take on only as much risk you can handle.

“When you have some money to invest, put it into low-cost, diversified index funds,” he said. “Find a stock-bond mix that you are comfortable with. And if you realize you’re not comfortable, change it until you are — and then stick with it for years, and do better things with your life than worrying about where the market is going.”

One way of thinking about risk is to imagine that a terrible downturn is about to occur, he said. “It will happen, if you live long enough. You can count on that.”

If you are a conservative, older investor, as he is, he said, you might consider a portfolio with 25 percent stocks and 75 percent bonds.

Consider the worst stock downturn in our lifetimes, from October 2007 through February 2009, he said.

In that horrendous period, when global markets fell 55 percent, this hypothetical conservative portfolio would have lost about 13.5 percent — and recovered all of the lost ground within 7 months. “When you look at the numbers,” he said, “you may think, ‘I can deal with that and sleep at night.’”

If you are younger or more aggressive in your investing, though, you might want to try a portfolio with more stock in it — say, 60 percent stock, with the remainder in bonds. But be aware that in the 2007-2009 market catastrophe, that portfolio would have lost about 35.6 percent and have required two years to recover entirely.

Because the bond market has been unusually strong, the conservative portfolio gained about 5.2 percent, annualized, over the 20 years through September; the more aggressive one gained slightly more, about 5.3 percent.

There are, of course, no guarantees that these returns will be duplicated in the future, Mr. Booth said.

“What this is, I think, is a reasonable approach to the future, based on the record of the past,” he said.

One thing it is not is a forecast.

-- Jeff Sommer, New York Times

Thursday, January 09, 2020

lessons from Buffett 1996

Warren Buffett (Trades, Portfolio)’s annual Berkshire Hathaway (NYSE:BRK.A)(NYSE:BRK.B) shareholder letters are filled with precious wisdom on investing, finance and business at large.

Below, we highlight a couple of takeaways that we feel are significantly meaningful even after decades, but rather underleveraged among today’s investing community.

Low-frequency wins

“Inactivity strikes us as intelligent behavior. Neither we nor most business managers would dream of feverishly trading highly-profitable subsidiaries because a small move in the Federal Reserve's discount rate was predicted or because some Wall Street pundit had reversed his views on the market. Why, then, should we behave differently with our minority positions in wonderful businesses? The art of investing in public companies successfully is little different from the art of successfully acquiring subsidiaries. In each case you simply want to acquire, at a sensible price, a business with excellent economics and able, honest management. Thereafter, you need only monitor whether these qualities are being preserved.”

Look for things that seldom change

“In studying the investments we have made in both subsidiary companies and common stocks, you will see that we favor businesses and industries unlikely to experience major change. The reason for that is simple: Making either type of purchase, we are searching for operations that we believe are virtually certain to possess enormous competitive strength ten or twenty years from now. A fast-changing industry environment may offer the chance for huge wins, but it precludes the certainty we seek.

Know your boundaries

“Should you choose, however, to construct your own portfolio, there are a few thoughts worth remembering. Intelligent investing is not complex, though that is far from saying that it is easy. What an investor needs is the ability to correctly evaluate selected businesses.

Note that word 'selected': You don't have to be an expert on every company, or even many. You only have to be able to evaluate companies within your circle of competence. The size of that circle is not very important; knowing its boundaries, however, is vital.

…

Your goal as an investor should simply be to purchase, at a rational price, a part interest in an easily-understandable business whose earnings are virtually certain to be materially higher five, ten and twenty years from now. Over time, you will find only a few companies that meet these standards - so when you see one that qualifies, you should buy a meaningful amount of stock. You must also resist the temptation to stray from your guidelines: If you aren't willing to own a stock for ten years, don't even think about owning it for ten minutes. Put together a portfolio of companies whose aggregate earnings march upward over the years, and so also will the portfolio's market value.”

Below, we highlight a couple of takeaways that we feel are significantly meaningful even after decades, but rather underleveraged among today’s investing community.

Low-frequency wins

“Inactivity strikes us as intelligent behavior. Neither we nor most business managers would dream of feverishly trading highly-profitable subsidiaries because a small move in the Federal Reserve's discount rate was predicted or because some Wall Street pundit had reversed his views on the market. Why, then, should we behave differently with our minority positions in wonderful businesses? The art of investing in public companies successfully is little different from the art of successfully acquiring subsidiaries. In each case you simply want to acquire, at a sensible price, a business with excellent economics and able, honest management. Thereafter, you need only monitor whether these qualities are being preserved.”

Look for things that seldom change

“In studying the investments we have made in both subsidiary companies and common stocks, you will see that we favor businesses and industries unlikely to experience major change. The reason for that is simple: Making either type of purchase, we are searching for operations that we believe are virtually certain to possess enormous competitive strength ten or twenty years from now. A fast-changing industry environment may offer the chance for huge wins, but it precludes the certainty we seek.

Know your boundaries

“Should you choose, however, to construct your own portfolio, there are a few thoughts worth remembering. Intelligent investing is not complex, though that is far from saying that it is easy. What an investor needs is the ability to correctly evaluate selected businesses.

Note that word 'selected': You don't have to be an expert on every company, or even many. You only have to be able to evaluate companies within your circle of competence. The size of that circle is not very important; knowing its boundaries, however, is vital.

…

Your goal as an investor should simply be to purchase, at a rational price, a part interest in an easily-understandable business whose earnings are virtually certain to be materially higher five, ten and twenty years from now. Over time, you will find only a few companies that meet these standards - so when you see one that qualifies, you should buy a meaningful amount of stock. You must also resist the temptation to stray from your guidelines: If you aren't willing to own a stock for ten years, don't even think about owning it for ten minutes. Put together a portfolio of companies whose aggregate earnings march upward over the years, and so also will the portfolio's market value.”

Tuesday, January 07, 2020

Just lucky I guess

The distribution of wealth follows a well-known pattern sometimes called an 80:20 rule: 80 percent of the wealth is owned by 20 percent of the people. Indeed, a report last year concluded that just eight men had a total wealth equivalent to that of the world’s poorest 3.8 billion people.

This seems to occur in all societies at all scales. It is a well-studied pattern called a power law that crops up in a wide range of social phenomena. But the distribution of wealth is among the most controversial because of the issues it raises about fairness and merit. Why should so few people have so much wealth?

The conventional answer is that we live in a meritocracy in which people are rewarded for their talent, intelligence, effort, and so on. Over time, many people think, this translates into the wealth distribution that we observe, although a healthy dose of luck can play a role.

What factors, then, determine how individuals become wealthy? Could it be that chance plays a bigger role than anybody expected? And how can these factors, whatever they are, be exploited to make the world a better and fairer place?

We finally get an answer thanks to the work of Alessandro Pluchino at the University of Catania in Italy and a couple of colleagues. These guys have created a computer model of human talent and the way people use it to exploit opportunities in life. The model allows the team to study the role of chance in this process.

The results are something of an eye-opener. Their simulations accurately reproduce the wealth distribution in the real world. But the wealthiest individuals are not the most talented (although they must have a certain level of talent). They are the luckiest. And this has significant implications for the way societies can optimize the returns they get for investments in everything from business to science.

This seems to occur in all societies at all scales. It is a well-studied pattern called a power law that crops up in a wide range of social phenomena. But the distribution of wealth is among the most controversial because of the issues it raises about fairness and merit. Why should so few people have so much wealth?

The conventional answer is that we live in a meritocracy in which people are rewarded for their talent, intelligence, effort, and so on. Over time, many people think, this translates into the wealth distribution that we observe, although a healthy dose of luck can play a role.

What factors, then, determine how individuals become wealthy? Could it be that chance plays a bigger role than anybody expected? And how can these factors, whatever they are, be exploited to make the world a better and fairer place?

We finally get an answer thanks to the work of Alessandro Pluchino at the University of Catania in Italy and a couple of colleagues. These guys have created a computer model of human talent and the way people use it to exploit opportunities in life. The model allows the team to study the role of chance in this process.

The results are something of an eye-opener. Their simulations accurately reproduce the wealth distribution in the real world. But the wealthiest individuals are not the most talented (although they must have a certain level of talent). They are the luckiest. And this has significant implications for the way societies can optimize the returns they get for investments in everything from business to science.

Thursday, January 02, 2020

2020: more normal?

(AP) — After a year of nirvana, investors may need to get ready for something a little more normal.

Markets are coming off a fabulous 2019, where stocks and bonds around the world climbed in concert. But for the next year — and decade, in fact — Wall Street is telling investors to set their expectations considerably lower.

It’s not calling for another crash like the U.S. stock market suffered just over a decade ago. Or for another run like the last 10 years, where the S&P 500 returned more than 13% on an annualized basis. A gain less than half of that may be more likely, both for next year and annually for the coming decade.

“People need to have a more realistic expectation of what returns are going to be,” said Greg Davis, chief investment officer at Vanguard. “That means investors who are saving for retirement or for college education will likely need to set aside more, because returns won’t be as generous as what we’ve seen over the last decade.”

It’s not because Wall Street sees the U.S. economy falling into a recession, at least not in 2020, even though that’s been a recurring fear for much of the last decade. Much of Wall Street expects the economy to chug modestly higher next year.

Instead, it’s a simple matter of math. Stocks and bonds don’t have as much room to rise after their stellar 2019, analysts say. Starting points matter, and investments began this year at a low point after recession worries pounded markets in December 2018. U.S. stocks will start 2020, meanwhile, close to their highest levels ever.

Wall Street has been busy trying to rein in expectations.

Vanguard forecasts U.S. stocks will return 3.5% to 5.5% annually over the coming decade. Even toward the top end of that range, it’s only half what the market has returned historically. Foreign stocks might offer a bit more, at roughly 7.5% annually, but U.S. bonds look set to offer only 2% or 3% annually over the next decade, according to Vanguard.

Of course, any prediction about where investments will end up is only a guess, no matter how educated. Many on Wall Street came into this year expecting only modest returns given all the worries about interest rates and a possible recession. Now, the S&P 500 is about to close out its second-best year of the last two decades.

Markets are coming off a fabulous 2019, where stocks and bonds around the world climbed in concert. But for the next year — and decade, in fact — Wall Street is telling investors to set their expectations considerably lower.

It’s not calling for another crash like the U.S. stock market suffered just over a decade ago. Or for another run like the last 10 years, where the S&P 500 returned more than 13% on an annualized basis. A gain less than half of that may be more likely, both for next year and annually for the coming decade.

“People need to have a more realistic expectation of what returns are going to be,” said Greg Davis, chief investment officer at Vanguard. “That means investors who are saving for retirement or for college education will likely need to set aside more, because returns won’t be as generous as what we’ve seen over the last decade.”

It’s not because Wall Street sees the U.S. economy falling into a recession, at least not in 2020, even though that’s been a recurring fear for much of the last decade. Much of Wall Street expects the economy to chug modestly higher next year.

Instead, it’s a simple matter of math. Stocks and bonds don’t have as much room to rise after their stellar 2019, analysts say. Starting points matter, and investments began this year at a low point after recession worries pounded markets in December 2018. U.S. stocks will start 2020, meanwhile, close to their highest levels ever.

Wall Street has been busy trying to rein in expectations.

Vanguard forecasts U.S. stocks will return 3.5% to 5.5% annually over the coming decade. Even toward the top end of that range, it’s only half what the market has returned historically. Foreign stocks might offer a bit more, at roughly 7.5% annually, but U.S. bonds look set to offer only 2% or 3% annually over the next decade, according to Vanguard.

Of course, any prediction about where investments will end up is only a guess, no matter how educated. Many on Wall Street came into this year expecting only modest returns given all the worries about interest rates and a possible recession. Now, the S&P 500 is about to close out its second-best year of the last two decades.

2019 stock market best since 2013

Wall Street closed the books Tuesday on a blockbuster 2019 for stock investors, with the broader market delivering its best returns in six years.

The S&P 500 finished with a gain of 28.9% for the year, while the Nasdaq composite rose 35.3%. For both indexes it was the best annual performance since 2013. Technology stocks helped power those gains by vaulting 48%.

The Dow Jones Industrial Average gained 22.3%, led by Apple.

Along the way, the three major indexes set more record highs than in 2018 and kept the longest bull market for stocks going.

”We had a remarkable year of returns in the stock market,” said Keith Buchanan, portfolio manager at Globalt Investments. “Things are much different going into 2020 than they were going into 2019.”

Wall Street’s record-shattering ride in 2019 was not without its bumps.

The market got off to a roaring start in January after Federal Reserve Chairman Jay Powell said the central bank would be “patient” with its interest rate policy following four increases in 2018. That encouraged investors who had been worried the Fed would continue hiking rates. Those concerns helped fuel a sell-off in the final quarter of 2018 that knocked the S&P 500 nearly 20% lower by December of that year.

With Muilenburg gone, attention turns to Boeing’s culture and engineering

US gains a robust 266,000 jobs; unemployment falls to 3.5%

January’s rally helped set the tone for a year in which the market responded to every downturn with a more sustained upswing. Along the way, stocks kept setting records — 35 of them for the S&P 500 index, 22 for the Dow and 31 for the Nasdaq.

By the end of the year, the Fed had completely reversed course and cut rates three times in what Powell called a pre-emptive move against any impact a sluggish global economy and the U.S.-China trade war might have on U.S. economic growth.

The market also overcame a late-summer slump caused by fears that the U.S. economy could be headed for a recession. Those concerns eased as investors drew encouragement from surprisingly good third-quarter corporate earnings and data showing the economy was not slowing as much as economists had feared.

“You fast-forward 12 months and now we’re going into 2020 and the sentiment seems like it’s fairly the opposite,” Buchanan said. ”There are fairly rosy expectations and there’s not a consensus that a recession is coming in a very near term.”

A truce in the 17-month U.S.-China trade war helped keep investors in a buying mood through the end of the year. Washington and Beijing announced in December they reached an agreement over a “Phase 1” trade deal that calls for the U.S. to reduce tariffs and China to buy larger quantities of U.S. farm products.

The S&P 500 finished with a gain of 28.9% for the year, while the Nasdaq composite rose 35.3%. For both indexes it was the best annual performance since 2013. Technology stocks helped power those gains by vaulting 48%.

The Dow Jones Industrial Average gained 22.3%, led by Apple.

Along the way, the three major indexes set more record highs than in 2018 and kept the longest bull market for stocks going.

”We had a remarkable year of returns in the stock market,” said Keith Buchanan, portfolio manager at Globalt Investments. “Things are much different going into 2020 than they were going into 2019.”

Wall Street’s record-shattering ride in 2019 was not without its bumps.

The market got off to a roaring start in January after Federal Reserve Chairman Jay Powell said the central bank would be “patient” with its interest rate policy following four increases in 2018. That encouraged investors who had been worried the Fed would continue hiking rates. Those concerns helped fuel a sell-off in the final quarter of 2018 that knocked the S&P 500 nearly 20% lower by December of that year.

With Muilenburg gone, attention turns to Boeing’s culture and engineering

US gains a robust 266,000 jobs; unemployment falls to 3.5%

January’s rally helped set the tone for a year in which the market responded to every downturn with a more sustained upswing. Along the way, stocks kept setting records — 35 of them for the S&P 500 index, 22 for the Dow and 31 for the Nasdaq.

By the end of the year, the Fed had completely reversed course and cut rates three times in what Powell called a pre-emptive move against any impact a sluggish global economy and the U.S.-China trade war might have on U.S. economic growth.

The market also overcame a late-summer slump caused by fears that the U.S. economy could be headed for a recession. Those concerns eased as investors drew encouragement from surprisingly good third-quarter corporate earnings and data showing the economy was not slowing as much as economists had feared.

“You fast-forward 12 months and now we’re going into 2020 and the sentiment seems like it’s fairly the opposite,” Buchanan said. ”There are fairly rosy expectations and there’s not a consensus that a recession is coming in a very near term.”

A truce in the 17-month U.S.-China trade war helped keep investors in a buying mood through the end of the year. Washington and Beijing announced in December they reached an agreement over a “Phase 1” trade deal that calls for the U.S. to reduce tariffs and China to buy larger quantities of U.S. farm products.

Monday, December 23, 2019

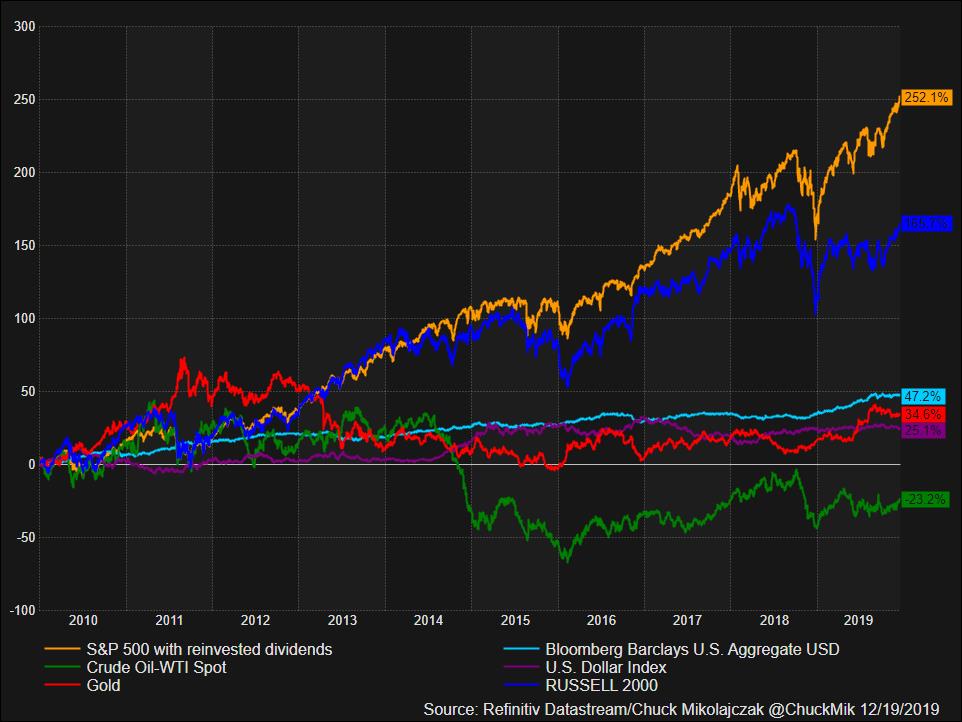

S&P 500 is the winner for the decade

NEW YORK (Reuters) - U.S. stocks are poised to close out the decade with the longest bull market in history still intact.

The run, which began on March 9, 2009, has narrowly avoided falling into a bear market several times over the past 10 years but for now appears on track to continue into next year.

With less than two weeks left in the decade, the large cap S&P 500, with reinvested dividends, has easily outperformed other major asset classes and benchmark commodities, climbing over 250%. The Bloomberg Barclays US Aggregate Bond Index .BCUSA, a broad-based index that includes Treasuries, corporate bonds and other fixed-income products, rose 47 percent. At the other end of the spectrum, WTI crude oil CLcv1 lost more than 20% over the same period.

(GRAPHIC: Asset performance for 2010-2019 - here)

Buoyed in part by an accommodative monetary policy from the Federal Reserve, which drove bond yields to near historic lows, the S&P 500 has been the best performing benchmark equity index over the decade out of the 10 largest global economies.

(GRAPHIC: U.S. stocks vs the world - here)

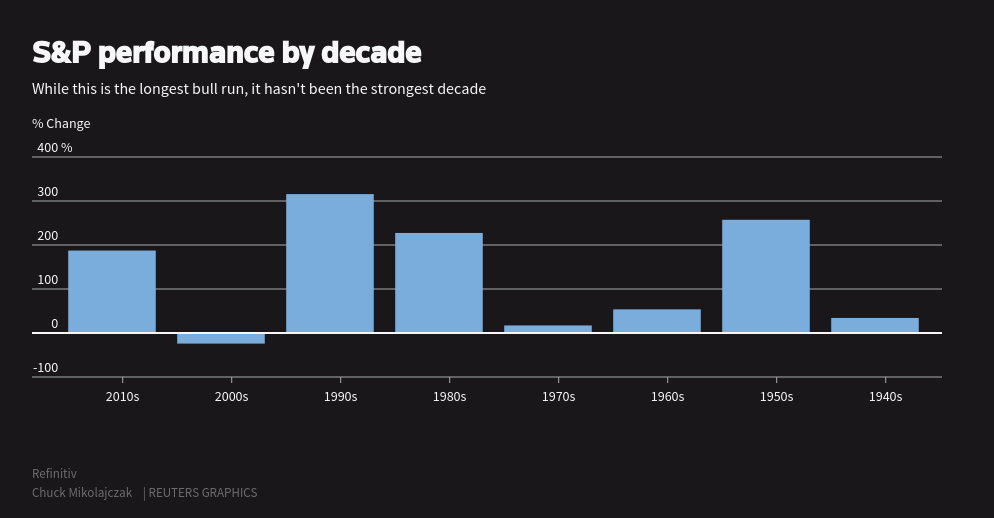

But while this has been the longest bull run on record, the Twenty-tens fell short of the showing for several prior decades for equities. The best of the past eight - dating to the 1940s - was the ‘90s, which topped 300%, followed by the ‘50s and the ‘80s, both north of 200%.

(GRAPHIC: S&P performance by decade - here)

The gains in the U.S. stock market were fueled by the technology .SPLRCT and consumer discretionary .SPLRCD sectors, with each climbing more than 300% over the decade. Energy .SPNY was the weakest group, narrowly avoiding a loss and was up only 4.3% through the Dec. 19 close.

(GRAPHIC: Sector performance for the decade - here)

While investors showed virtually no preference between growth .RAG or value .RAV stocks in the early years of the decade, growth as an investing style has handily outperformed value stocks in the last leg of the ‘10s.

(GRAPHIC: Growth vs value stocks for the decade - here)

The preference for growth names is also reflected in the performance of individual stocks over the decade, led by the gain in Netflix (NFLX.O), which notched a staggering 4100% through the Dec. 19 close.

(GRAPHIC: Top S&P 500 performers of the decade - here)

Bringing up the rear were several energy names, with Apache (APA.N) suffering the worst performance, down nearly 80% over the 10-year time frame.

The run, which began on March 9, 2009, has narrowly avoided falling into a bear market several times over the past 10 years but for now appears on track to continue into next year.

With less than two weeks left in the decade, the large cap S&P 500, with reinvested dividends, has easily outperformed other major asset classes and benchmark commodities, climbing over 250%. The Bloomberg Barclays US Aggregate Bond Index .BCUSA, a broad-based index that includes Treasuries, corporate bonds and other fixed-income products, rose 47 percent. At the other end of the spectrum, WTI crude oil CLcv1 lost more than 20% over the same period.

(GRAPHIC: Asset performance for 2010-2019 - here)

{kind=link}

Buoyed in part by an accommodative monetary policy from the Federal Reserve, which drove bond yields to near historic lows, the S&P 500 has been the best performing benchmark equity index over the decade out of the 10 largest global economies.

(GRAPHIC: U.S. stocks vs the world - here)

{kind=link}

But while this has been the longest bull run on record, the Twenty-tens fell short of the showing for several prior decades for equities. The best of the past eight - dating to the 1940s - was the ‘90s, which topped 300%, followed by the ‘50s and the ‘80s, both north of 200%.

(GRAPHIC: S&P performance by decade - here)

{kind=link}

The gains in the U.S. stock market were fueled by the technology .SPLRCT and consumer discretionary .SPLRCD sectors, with each climbing more than 300% over the decade. Energy .SPNY was the weakest group, narrowly avoiding a loss and was up only 4.3% through the Dec. 19 close.

(GRAPHIC: Sector performance for the decade - here)

{kind=link}

While investors showed virtually no preference between growth .RAG or value .RAV stocks in the early years of the decade, growth as an investing style has handily outperformed value stocks in the last leg of the ‘10s.

(GRAPHIC: Growth vs value stocks for the decade - here)

{kind=link}

The preference for growth names is also reflected in the performance of individual stocks over the decade, led by the gain in Netflix (NFLX.O), which notched a staggering 4100% through the Dec. 19 close.

(GRAPHIC: Top S&P 500 performers of the decade - here)

{kind=link}

Friday, December 06, 2019

best retirement stocks

From a Kiplinger article titled 20 best retirement stocks to buy in 2020

These are stocks with relative good dividends plus a history of dividend growth

Among those that caught my eye:

Stock Yield Growth streak

Flowers Food (FLO) 3.5% 17 years

Realty Income (O) 3.6% 30 years

National Retail Properties (NNN) 3.7% 30 years

Verizon (VZ) 4.1% 13 years

Duke Energy (DUK) 4.3% 15 years

Dominion Energy (D) 4.5% 16 years

Telus (TU) 4.7% 17 years

Exxon Mobil (XOM) 5.1% 37 years

W.P. Carey (WPC) 5.1% 20 years

Oneok (OKE) 5.2% 17 years

National Health Investors 5.2% 10 years

AT&T (T) 5.4% 35 years

These are stocks with relative good dividends plus a history of dividend growth

Among those that caught my eye:

Stock Yield Growth streak

Flowers Food (FLO) 3.5% 17 years

Realty Income (O) 3.6% 30 years

National Retail Properties (NNN) 3.7% 30 years

Verizon (VZ) 4.1% 13 years

Duke Energy (DUK) 4.3% 15 years

Dominion Energy (D) 4.5% 16 years

Telus (TU) 4.7% 17 years

Exxon Mobil (XOM) 5.1% 37 years

W.P. Carey (WPC) 5.1% 20 years

Oneok (OKE) 5.2% 17 years

National Health Investors 5.2% 10 years

AT&T (T) 5.4% 35 years

Monday, November 04, 2019

Howard Marks 20 important things

Part 1 of 4

1. Second Level Thinking

2. understanding market efficiency

3. value

4. the relationship between value and price

5. understanding risk

Part II of IV

6. recognizing risk

7. controlling rik

8. be attentive to cycles

9. awareness of the pendulum

10. combating negative influences

Part III of IV

Part IV of IV

the original pdf

the book

11/4/19 - Altucher interview

[originally posted 9/7/13, updated 1/22/20]

1. Second Level Thinking

2. understanding market efficiency

3. value

4. the relationship between value and price

5. understanding risk

Part II of IV

6. recognizing risk

7. controlling rik

8. be attentive to cycles

9. awareness of the pendulum

10. combating negative influences

Part III of IV

Part IV of IV

the original pdf

the book

11/4/19 - Altucher interview

[originally posted 9/7/13, updated 1/22/20]

Sunday, October 20, 2019

5 signs you're a value investor

1. You are obsessed with Warren Buffett

Do you watch every interview on CNBC that Buffett does?

Do you read every one of Berkshire’s shareholder letters, attend the annual meetings because you’re a shareholder, or quote Buffett on social media?

An obsession with Mr. Buffett is one big sign that you’re probably a value investor yourself.

2. You love stocks trading at 52-week lows

Benjamin Graham, the father of value investing, has told investors to look for stocks trading on new 52-week lows.

If you enjoy looking at those stocks because you’re thinking you’re getting a bargain, you could be a value investor.

3. You buy and hold your stocks

Buffett has owned some of his stocks for decades. Have you? If so, you may also be a value investor.

4. You love “boring” companies

Buffett has gotten rich owning some of the more “boring” types of companies including industrials, railroads, energy and, famously, insurance.

5. You never buy companies with negative earnings

If you don’t understand what all the fuss is about with Uber or Lyft, both of which don’t have positive earnings, you may be a value investor.

Do you watch every interview on CNBC that Buffett does?

Do you read every one of Berkshire’s shareholder letters, attend the annual meetings because you’re a shareholder, or quote Buffett on social media?

An obsession with Mr. Buffett is one big sign that you’re probably a value investor yourself.

2. You love stocks trading at 52-week lows

Benjamin Graham, the father of value investing, has told investors to look for stocks trading on new 52-week lows.

If you enjoy looking at those stocks because you’re thinking you’re getting a bargain, you could be a value investor.

3. You buy and hold your stocks

Buffett has owned some of his stocks for decades. Have you? If so, you may also be a value investor.

4. You love “boring” companies

Buffett has gotten rich owning some of the more “boring” types of companies including industrials, railroads, energy and, famously, insurance.

5. You never buy companies with negative earnings

If you don’t understand what all the fuss is about with Uber or Lyft, both of which don’t have positive earnings, you may be a value investor.

Tuesday, October 08, 2019

major selloff predicted

The technical analysis that correctly called the market bottom in December is now calling a top in the S&P 500, CNBC's Jim Cramer said Tuesday.

The "Mad Money" host said a colleague of his at RealMoney.com is warning that "we're really cruising for a bruising" beyond the 1.56% decline Tuesday by the index.

Bob Moreno, chartist at RightViewTrading.com who projected in February that the market had more room to run, warns of a possible plummet in the large-cap index.

"Now those same charts tell Moreno that we're approaching an important moment and he's predicting a major sell-off from these levels, a 10% decline in the S&P," Cramer said.

That would bring the S&P below 2,620 from its 2,893.06 Tuesday close.

Since its low following the major December sell-off, the S&P 500 has gained about 27%. The index made a series of higher highs and higher lows during that expansion, but Moreno is convinced that momentum was disrupted in September when it produced a lower high, Cramer explained perusing the weekly chart of the S&P 500.

According to FactSet, the S&P 500 posted a closing high of 3,025.86 in late July and failed to break past 3,010 in September, a potential peak. Moreno, Cramer said, determined that to be a "double top," which is a bearish technical reversal pattern.

"Moreno believes the S&P is going to test its floor of support again, only this time that floor is at 2,825," Cramer said. "But if it fails, and he thinks it will, another floor at 2,725. That's where the S&P bottomed in March and June."

"Unfortunately, he doesn't see that trading floor ... holding either," Cramer said. "If the S&P breaks down from the current consolidation pattern, we could have not a little but a lot more downside."

There are more bearish indicators in Moreno's analysis. He notes the Moving Average Convergence Divergence indicator had a bearish crossover, which means momentum is slowing, and the Chaikin Oscillator supply/demand indicator dropped below its center line, which means money flow is negative, Cramer said.

"He's hoping the S&P 500 can find a floor at the 2,600 level. ... That's still a long way from a retest of last December's lows, but it's pretty horrible," he said. If the floor at 2,600 fails, Moreno "did say when we talked to him that if this fails, we could revisit [the December] level."

Chartists analyze past price action in stocks to forecast future price direction.

"Do I agree? Moreno's views echo my own for vast swathes of the market, but as someone who likes individual stocks, I'm ready for chance to buy best-of-breed names at bargain basement prices," Cramer said.

***

So he's predicting a floor at 2825, another floor at 2725, and another floor at 2600. Then I guess 2350 which is where the December low was. Well, that narrows it down...

I'd be looking to buy at each floor because nobody really knows which floor is actually going to hold.

***

Looking at the chart, I'd be looking to buy at around 2850 which is near the August bottom and the 200-day MA. Then I'd look to buy at around 2750 which is near the beginning of June low. Then maybe 2650 which is around the Oct/Nov 2018 lows. Then around 2400 as it approaches the December low. Maybe one of those will prove to be the bottom.

The "Mad Money" host said a colleague of his at RealMoney.com is warning that "we're really cruising for a bruising" beyond the 1.56% decline Tuesday by the index.

Bob Moreno, chartist at RightViewTrading.com who projected in February that the market had more room to run, warns of a possible plummet in the large-cap index.

"Now those same charts tell Moreno that we're approaching an important moment and he's predicting a major sell-off from these levels, a 10% decline in the S&P," Cramer said.

That would bring the S&P below 2,620 from its 2,893.06 Tuesday close.

Since its low following the major December sell-off, the S&P 500 has gained about 27%. The index made a series of higher highs and higher lows during that expansion, but Moreno is convinced that momentum was disrupted in September when it produced a lower high, Cramer explained perusing the weekly chart of the S&P 500.

According to FactSet, the S&P 500 posted a closing high of 3,025.86 in late July and failed to break past 3,010 in September, a potential peak. Moreno, Cramer said, determined that to be a "double top," which is a bearish technical reversal pattern.

"Moreno believes the S&P is going to test its floor of support again, only this time that floor is at 2,825," Cramer said. "But if it fails, and he thinks it will, another floor at 2,725. That's where the S&P bottomed in March and June."

"Unfortunately, he doesn't see that trading floor ... holding either," Cramer said. "If the S&P breaks down from the current consolidation pattern, we could have not a little but a lot more downside."

There are more bearish indicators in Moreno's analysis. He notes the Moving Average Convergence Divergence indicator had a bearish crossover, which means momentum is slowing, and the Chaikin Oscillator supply/demand indicator dropped below its center line, which means money flow is negative, Cramer said.

"He's hoping the S&P 500 can find a floor at the 2,600 level. ... That's still a long way from a retest of last December's lows, but it's pretty horrible," he said. If the floor at 2,600 fails, Moreno "did say when we talked to him that if this fails, we could revisit [the December] level."

Chartists analyze past price action in stocks to forecast future price direction.

"Do I agree? Moreno's views echo my own for vast swathes of the market, but as someone who likes individual stocks, I'm ready for chance to buy best-of-breed names at bargain basement prices," Cramer said.

***

So he's predicting a floor at 2825, another floor at 2725, and another floor at 2600. Then I guess 2350 which is where the December low was. Well, that narrows it down...

I'd be looking to buy at each floor because nobody really knows which floor is actually going to hold.

***

Looking at the chart, I'd be looking to buy at around 2850 which is near the August bottom and the 200-day MA. Then I'd look to buy at around 2750 which is near the beginning of June low. Then maybe 2650 which is around the Oct/Nov 2018 lows. Then around 2400 as it approaches the December low. Maybe one of those will prove to be the bottom.

Tuesday, October 01, 2019

Schwab eliminates commissions

Almost forty five years ago, Chuck Schwab made investing more accessible to all Americans with the concept of low commissions to buy and sell stocks. On October 7, 2019, in conjunction with the release of Mr. Schwab’s latest book, “Invested,” Charles Schwab & Co., Inc. is removing the final barrier to making investing accessible to everyone by eliminating commissions for stocks, ETFs and options listed on U.S. or Canadian exchanges, across all mobile and web trading channels1. Clients trading options will continue to pay 65 cents per contract.

Founder and Chairman Charles Schwab said, “From day one, my passion has been to make investing easier and more affordable for everyone. Beginning October 7, every Schwab client can trade U.S. stocks, ETFs and options commission-free. Eliminating commissions ensures my ultimate vision is realized – making investing accessible to all.”

Schwab CEO and President Walt Bettinger emphasized, “This is our price. Not a promotion. No catches. Period. Price should never be a barrier to investing for anyone, whether an experienced investor or someone just starting on the investing path. We’re proud to provide clients with a full-service, modern investing experience that delivers on our no trade-offs combination of service, simplicity and superior value – backed by a satisfaction guarantee2. In support of the valued independent investment advisors we serve, the same pricing will apply to their clients when trading at Schwab.”

Beginning October 7, 2019, the company will reduce U.S. stock, ETF and options online trade commissions from $4.95 to zero. And with no minimum account size3 to open a full featured Schwab brokerage account, every investor, no matter how large or small, can benefit from the expertise and support of a firm that has been entrusted with more than $3.7 trillion in client assets. Every Schwab client using our web and mobile channels automatically qualifies for the new pricing, without opening a new account, making a new deposit or maintaining a minimum balance of any type.

***

[10/3/19] ETrade follows TD Ameritrade in announcing zero commissions.

But what about Fidelity?

[10/12/19] Fidelity cuts fees to $0

Founder and Chairman Charles Schwab said, “From day one, my passion has been to make investing easier and more affordable for everyone. Beginning October 7, every Schwab client can trade U.S. stocks, ETFs and options commission-free. Eliminating commissions ensures my ultimate vision is realized – making investing accessible to all.”

Schwab CEO and President Walt Bettinger emphasized, “This is our price. Not a promotion. No catches. Period. Price should never be a barrier to investing for anyone, whether an experienced investor or someone just starting on the investing path. We’re proud to provide clients with a full-service, modern investing experience that delivers on our no trade-offs combination of service, simplicity and superior value – backed by a satisfaction guarantee2. In support of the valued independent investment advisors we serve, the same pricing will apply to their clients when trading at Schwab.”

Beginning October 7, 2019, the company will reduce U.S. stock, ETF and options online trade commissions from $4.95 to zero. And with no minimum account size3 to open a full featured Schwab brokerage account, every investor, no matter how large or small, can benefit from the expertise and support of a firm that has been entrusted with more than $3.7 trillion in client assets. Every Schwab client using our web and mobile channels automatically qualifies for the new pricing, without opening a new account, making a new deposit or maintaining a minimum balance of any type.

***

[10/3/19] ETrade follows TD Ameritrade in announcing zero commissions.

But what about Fidelity?

[10/12/19] Fidelity cuts fees to $0

Monday, August 19, 2019

Seth Klarman on buying

[4/26/17] Position sizing is another important part of portfolio management. Different stocks can command different percentages of your investment portfolio, depending on conviction. Klarman believes one of the best strategies to build a position, as well as an understanding of the business you are investing in, is to build a new position gradually:

“The single most crucial factor in trading is developing the appropriate reaction to price fluctuations…One half of trading involves learning how to buy. In my view, investors should usually refrain from purchasing a 'full position' (the maximum dollar commitment they intend to make) in a given security all at once…Buying a partial position leaves reserves that permit investors to 'average down,' lowering their average cost per share, if prices decline…If the security you are considering is truly a good investment, not a speculation, you would certainly want to own more at lower prices. If, prior to purchase, you realize that you are unwilling to average down, then you probably should not make the purchase in the first place.”

[12/13/17 - waiting for the bottom?]

“While it is always tempting to try to time the market and wait for the bottom to be reached (as if it would be obvious when it arrived), such a strategy has proven over the years to be deeply flawed...the price recovery from a bottom can be very swift. Therefore, an investor should put money to work amidst the throes of a bear market, appreciating that things will likely get worse before they get better.”

[12/3/18] Seth Klarman's 3 Pillars of Investing

[8/19/19] “In a market downturn, momentum investors cannot find momentum, growth investors worry about a slowdown, and technical analysts don't like their charts. But the value investing discipline tells you exactly what to analyze, price versus value, and then what to do, buy at a considerable discount and sell near full value.

And, because you cannot tell what the market is going to do, a value investment discipline is important because it is the only approach that produces consistently good investment results over a complete market cycle.”

“The single most crucial factor in trading is developing the appropriate reaction to price fluctuations…One half of trading involves learning how to buy. In my view, investors should usually refrain from purchasing a 'full position' (the maximum dollar commitment they intend to make) in a given security all at once…Buying a partial position leaves reserves that permit investors to 'average down,' lowering their average cost per share, if prices decline…If the security you are considering is truly a good investment, not a speculation, you would certainly want to own more at lower prices. If, prior to purchase, you realize that you are unwilling to average down, then you probably should not make the purchase in the first place.”

[12/13/17 - waiting for the bottom?]

“While it is always tempting to try to time the market and wait for the bottom to be reached (as if it would be obvious when it arrived), such a strategy has proven over the years to be deeply flawed...the price recovery from a bottom can be very swift. Therefore, an investor should put money to work amidst the throes of a bear market, appreciating that things will likely get worse before they get better.”

[12/3/18] Seth Klarman's 3 Pillars of Investing

[8/19/19] “In a market downturn, momentum investors cannot find momentum, growth investors worry about a slowdown, and technical analysts don't like their charts. But the value investing discipline tells you exactly what to analyze, price versus value, and then what to do, buy at a considerable discount and sell near full value.

And, because you cannot tell what the market is going to do, a value investment discipline is important because it is the only approach that produces consistently good investment results over a complete market cycle.”

Friday, August 02, 2019

Trump vs. China

[8/2/19] BEIJING/WASHINGTON (Reuters) - China on Friday vowed to fight back

against U.S. President Donald Trump’s abrupt decision to slap 10%

tariffs on the remaining $300 billion in Chinese imports, a move that

ended a month-long trade truce.

China’s new ambassador to the United Nations, Zhang Jun, said Beijing would take “necessary countermeasures” to protect its rights and bluntly described Trump’s move as “an irrational, irresponsible act.”

“China’s position is very clear that if U.S. wishes to talk, then we will talk, if they want to fight, then we will fight,” Zhang told reporters in New York, also signalling that trade tensions could hurt cooperation between the countries on dealing with North Korea.

Trump said China had to do a lot in order to turn things around in the trade talks and repeated an earlier threat to substantially increase tariffs if they failed to do so.

“We can’t just go and make an even deal with China. We have to go and make a better deal with China,” Trump told reporters at the White House.

The U.S. president stunned financial markets on Thursday by saying he plans to levy the additional duties starting Sept. 1, marking a sudden end to a truce in a year-long trade war between the world’s two biggest economies that has slowed global growth and disrupted supply chains.

U.S. stocks extended their sell-off Friday on Trump’s tariff announcement. Yields on U.S. and German debt plumbed multi-year lows amid a rush for safe-haven assets.

Earlier on Friday, Chinese Foreign Ministry spokeswoman Hua Chunying said China was holding firm to its position in the 13-month tariff brawl with the United States.

“We won’t accept any maximum pressure, intimidation or blackmail,” Hua told a news briefing in Beijing.

“On the major issues of principle we won’t give an inch,” she said, adding that China hoped the United States would “give up its illusions” and return to negotiations based on mutual respect and equality.

Retaliatory measures by China could include tariffs, a ban on the export of rare earths that are used in everything from military equipment to consumer electronics, and penalties against U.S. companies in China, according to analysts.

Trump also threatened to further raise tariffs if Chinese President Xi Jinping fails to move more quickly to strike a trade deal.

The 10% duties, which Trump announced in a series of Twitter posts after his top trade negotiators briefed him on a lack of progress in talks in Shanghai this week, would extend tariffs to nearly all Chinese goods that the United States imports.

China’s new ambassador to the United Nations, Zhang Jun, said Beijing would take “necessary countermeasures” to protect its rights and bluntly described Trump’s move as “an irrational, irresponsible act.”

“China’s position is very clear that if U.S. wishes to talk, then we will talk, if they want to fight, then we will fight,” Zhang told reporters in New York, also signalling that trade tensions could hurt cooperation between the countries on dealing with North Korea.

Trump said China had to do a lot in order to turn things around in the trade talks and repeated an earlier threat to substantially increase tariffs if they failed to do so.

“We can’t just go and make an even deal with China. We have to go and make a better deal with China,” Trump told reporters at the White House.

The U.S. president stunned financial markets on Thursday by saying he plans to levy the additional duties starting Sept. 1, marking a sudden end to a truce in a year-long trade war between the world’s two biggest economies that has slowed global growth and disrupted supply chains.

U.S. stocks extended their sell-off Friday on Trump’s tariff announcement. Yields on U.S. and German debt plumbed multi-year lows amid a rush for safe-haven assets.

Earlier on Friday, Chinese Foreign Ministry spokeswoman Hua Chunying said China was holding firm to its position in the 13-month tariff brawl with the United States.

“We won’t accept any maximum pressure, intimidation or blackmail,” Hua told a news briefing in Beijing.

“On the major issues of principle we won’t give an inch,” she said, adding that China hoped the United States would “give up its illusions” and return to negotiations based on mutual respect and equality.

Retaliatory measures by China could include tariffs, a ban on the export of rare earths that are used in everything from military equipment to consumer electronics, and penalties against U.S. companies in China, according to analysts.

Trump also threatened to further raise tariffs if Chinese President Xi Jinping fails to move more quickly to strike a trade deal.

The 10% duties, which Trump announced in a series of Twitter posts after his top trade negotiators briefed him on a lack of progress in talks in Shanghai this week, would extend tariffs to nearly all Chinese goods that the United States imports.

Tuesday, July 02, 2019

rich get richer

Welcome to the longest U.S. economic expansion in history, one

perhaps best characterized by the excesses of extreme wealth and an

ever-widening chasm between the unfathomably rich and everyone else.

Indeed, as the expansion entered its record-setting 121st month on Monday, signs of a new Gilded Age are all over.

Big-money deals are getting bigger, from corporate mergers and acquisitions, to individuals buying luxury penthouses, sports teams, yachts and all-frills pilgrimages to the ends of the earth. And while these deals grab headlines, there is a deeper trend at work. The number of billionaires in the United States has more than doubled in the last decade, from 267 in 2008 to 607 last year, according to UBS.

“The rich have gotten richer and they’ve gotten richer faster,” said John Mathews, Head of Private Wealth Management and Ultra High Net Worth at UBS (UBSG.S) Global Wealth Management. “The drive or the desire for consumption has just gone upscale.”

But there are also signs of struggle and stagnation at lower-income levels. The wealthiest fifth of Americans hold 88% of the country’s wealth, a share that has grown since before the crisis, Federal Reserve data through 2016 shows. Meanwhile, the number of people receiving federal food stamps tops 39 million, below the peak in 2013 but still up 40% from 2008 even though the country’s population has only grown about 8%.

Anger over what some see as the unfairness of the economy has bubbled into the country’s politics, with Democratic presidential candidates promising to lower healthcare costs, guarantee jobs and tax the rich.

Indeed, as the expansion entered its record-setting 121st month on Monday, signs of a new Gilded Age are all over.

Big-money deals are getting bigger, from corporate mergers and acquisitions, to individuals buying luxury penthouses, sports teams, yachts and all-frills pilgrimages to the ends of the earth. And while these deals grab headlines, there is a deeper trend at work. The number of billionaires in the United States has more than doubled in the last decade, from 267 in 2008 to 607 last year, according to UBS.

“The rich have gotten richer and they’ve gotten richer faster,” said John Mathews, Head of Private Wealth Management and Ultra High Net Worth at UBS (UBSG.S) Global Wealth Management. “The drive or the desire for consumption has just gone upscale.”

But there are also signs of struggle and stagnation at lower-income levels. The wealthiest fifth of Americans hold 88% of the country’s wealth, a share that has grown since before the crisis, Federal Reserve data through 2016 shows. Meanwhile, the number of people receiving federal food stamps tops 39 million, below the peak in 2013 but still up 40% from 2008 even though the country’s population has only grown about 8%.

Anger over what some see as the unfairness of the economy has bubbled into the country’s politics, with Democratic presidential candidates promising to lower healthcare costs, guarantee jobs and tax the rich.

Saturday, June 22, 2019

Facebook and Libra

Believe it or not, Facebook will be the company that brings cryptocurrency to the masses. Today the social network giant published detailed plans for a cryptocurrency called libra, backed by currencies from the most trusted central banks around the world, and accessible even without a bank account.

But for Facebook, a company that generated $55.8 billion revenue in 2018, almost exclusively by monetizing a shared social network, the push into blockchain, a shared financial network of transactions, represents multiple possible new revenue streams. Ultimately Facebook could reap rewards from financial services it may offer via a new crypto subsidiary called Calibra as well as the income it might generate if its vast customer base parks funds in its reserves backing its new coin.

With plans to integrate its own cryptocurrency wallet in with Facebook-owned WhatsApp and Messenger when the cryptocurrency goes live in 2020, Facebook will instantly bridge the world’s largest social network with the brave new world of cryptocurrency. All that’s left is for users to use it.

Friday, June 14, 2019

Social Security facing shortfall

A slow-moving